From Redlining to Racial Justice

Beneficial State Foundation

May 30, 2025

Introduction

Though rooted in the past, redlining’s legacy continues to shape financial realities for communities of color today. Redlining refers to the discriminatory practice, formalized in the 1930s, where banks and government agencies denied mortgages or insurance to people based on the racial or ethnic composition of their neighborhoods—literally outlining “undesirable” areas in red on maps.

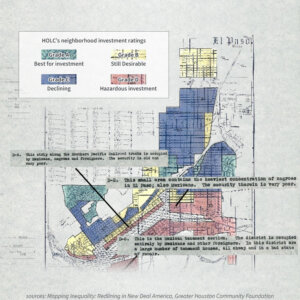

This system originated with the creation of the Home Owners Loan Corporation (HOLC) in 1933, a federal agency meant to prevent foreclosures during the Great Depression by refinancing mortgages. HOLC created “residential security” maps to guide investment decisions, and in doing so, directed public and private capital to predominantly white neighborhoods—while systematically devaluing areas where Black, immigrant, and communities of color lived, reinforcing segregation. These policies institutionalized segregation, limited access to homeownership, and deepened racial wealth gaps that persist to this day.

Although redlining was outlawed by the Fair Housing Act of 1968, its effects remain deeply embedded in our financial institutions and housing markets. Today, regulators, banks, and advocates are working to reverse this damage. Through research that uncovers the long-term effects of disinvestment, and through regulatory measures that hold lenders accountable, a new chapter in the fight for racial equity in banking is emerging. These efforts recognize that achieving financial fairness means addressing historic harm through targeted reinvestment and systemic change.

The Lasting Impact of Redlining

Despite legal reforms, once redlined neighborhoods still receive fewer mortgages compared to those rated favorably by the Home Owners Loan Corporation (HOLC). Using a new HMDA Longitudinal Dataset (HLD), the National Community Reinvestment Coalition’s (NCRC) Decades of Disinvestment report provides specific evidence of how these areas remain underserved by lenders, perpetuating racial and economic gaps in homeownership.

The study explores the long-term effects of historic redlining on mortgage lending, focusing on disparities in mortgage originations across neighborhoods since 1981. Using the HMDA Longitudinal Dataset and a Historic Redlining Indicator, it finds that neighborhoods previously rated as “Hazardous” by HOLC continue to receive fewer mortgage loans than those rated as “Best,” even after accounting for housing market factors.

These ratings—originally detailed in HOLC’s “residential security” maps—can be explored at Mapping Inequality: Redlining in New Deal America, which digitizes the area descriptions used to justify these designations.

The research emphasizes that structural racism and residential segregation are deeply embedded in the U.S. housing finance system, keeping redlined neighborhoods economically disadvantaged and limiting their access to mortgage credit. This ongoing discrimination widens the racial wealth gap and reinforces systemic inequality.

Current Efforts and Lessons Learned

Recent efforts to combat the effects of redlining have seen significant developments. The American Bankers Association’s Risk and Compliance Magazine, in its July-August 2024 issue, sheds light on the ongoing challenges and new strategies in redlining enforcement. Since the launch of the Combating Redlining Initiative in 2021, the Department of Justice (DOJ) has initiated numerous investigations and settlements, resulting in over $150 million in relief for affected communities.

These initiatives underscore the need for strategies tailored to each community’s unique demographics. While the banking industry has a long way to go to remedy redlining’s harmful legacy, there are a few practices that all financial institutions should be doing today.

- Evaluation: Recommendations for banks include routinely analyzing lending patterns across neighborhoods, tracking and improving performance in majority-minority areas over time, and benchmarking this performance against the rest of their portfolio and those of peer institutions.

- Presence: Banks should regularly assess branch locations and referral sources to evaluate whether their physical presence and partner networks equitably serve communities of color, rather than being concentrated in predominantly white areas.

- Product Design: Banks can increase access to helpful financial services for families historically denied wealth-building through home equity by designing products and services that address their specific financial situations, such as changing collateral or downpayment requirements.

- Appraisals: Banks should ensure that relevant staff members are trained on appraisal bias and the chronic undervaluation of homes in redlined neighborhoods. They should enact measures to detect and correct unfair appraisals so that homeowners and sellers of color can benefit from the full and fair value of their homes.

- Outreach: Additionally, banks should assess whether their marketing and outreach efforts effectively reach underserved markets to help close longstanding gaps in access to financial services.

For more insight into effective practices, the ABA Banking Journal’s article on Lessons Learned from the Initiative to Combat Redlining provides practical guidance for banks aiming to improve their minority market lending performance. Our colleagues have also contributed to this dialogue, making a credible case for diversity, equity, and inclusion (DEI) in the banking industry in their piece, DEI Delivers for Banks.

Our Commitment: Underwriting for Racial Justice

At Beneficial State Foundation, we are dedicated to developing initiatives that promote racial equity in banking. One of our key initiatives is Underwriting for Racial Justice, which helps banks explore the development of Special Purpose Credit Programs (SPCPs). These programs are designed to provide targeted financial products to historically underserved communities, aligning with recommendations from the “Lessons Learned” article.

Join Us in Advancing Equitable Bank Standards

We invite you to learn more about our initiatives, including Underwriting for Racial Justice and our Equitable Bank Standards. Together, we can work towards a banking system that goes beyond repairing past harm by truly serving all communities into the future. Follow us on social media (LinkedIn, Facebook, Instagram, X, and Bluesky), and stay tuned for updates and insights as we continue to advocate for a more just banking system.